Current Study: One in Three Retailers Anticipates Restructuring by Year-End / Jobs to Be Cut and Stores Closed

December 7, 2024

- New Insight

Results of a recent survey by Verian (formerly Kantar Public) conducted on behalf of FTI-Andersch in the Automotive, Machinery and Plant Engineering, Consumer Goods, and Retail Sectors:

- 17% of respondents planning restructuring foresee store closures.

- In the medium term, nearly 46% of companies aim to carry out restructuring.

- 91% of respondents face challenges related to labor shortages, despite planned job cuts.

Overall, the non-food retail sector in Germany assesses its economic situation more negatively than the industrial sector. Almost half (48%) of retailers expect worse business performance compared to the previous year (vs. 34% in industry), 60% anticipate an increase in insolvencies in the retail sector (vs. 42% in industry), and one in three retailers (34%) expects a "wave of insolvencies" (vs. 21% in industry) among retailers and suppliers. A quarter of respondents (24%) consider themselves "existentially threatened" if industry-wide insolvencies occur as expected (vs. 9% in industry).

"Insolvencies can quickly trigger a domino effect: customers and suppliers disappear, price wars escalate, financiers grow increasingly skeptical, and the attractiveness of city centers continues to decline," says Dorothée Fritsch, Managing Director and retail expert at FTI-Andersch, the restructuring, business transformation, and transaction consulting unit of FTI Consulting in Germany.

"We have already seen the first prominent insolvencies. Now, structural challenges are colliding with what is likely the worst economic situation since the financial crisis, combined with persistently weak consumer sentiment. Recently, in addition to vertical integrators and platform operators, more international players have aggressively entered the German market. The result: market consolidation is inevitable," says Fritsch.

FTI-Andersch Expert: Net Job Losses Expected in Retail

One-third (36%) of retail companies already undergoing restructuring are actively reducing jobs. Half (50%) of respondents currently considering restructuring plan workforce reductions. At the same time, the biggest hurdle to a successful realignment is workforce retention and recruitment—cited by 84% of retail companies currently planning or undergoing restructuring.

Retail faces greater challenges in this area compared to the industrial sector. Among those already in restructuring, 91% report difficulties in retaining and recruiting employees. In the industrial sector, only two-thirds (66%) of respondents identify this as a significant issue.

"At the point of sale (POS), retailers need sales staff with higher qualifications to meet increased customer expectations. Everyone is competing for these top professionals, and the labor shortage has been significantly exacerbated by the COVID-19 pandemic," says Dorothée Fritsch. "Additionally, there is a lack of experts in digitalization, supply chain management, and innovation."

Another major challenge for retailers is refinancing. This is partly due to the current interest rate environment and partly to increased requirements from financiers as a result of structural market changes. Consequently, two-thirds (66%) of retailers face major or very major challenges in refinancing, compared to less than half (45%) of industrial companies. Despite this, half (48%) of retail companies with short-term refinancing needs are not increasing communication with their financiers.

Simultaneous Stability and Strategic Realignment Necessary

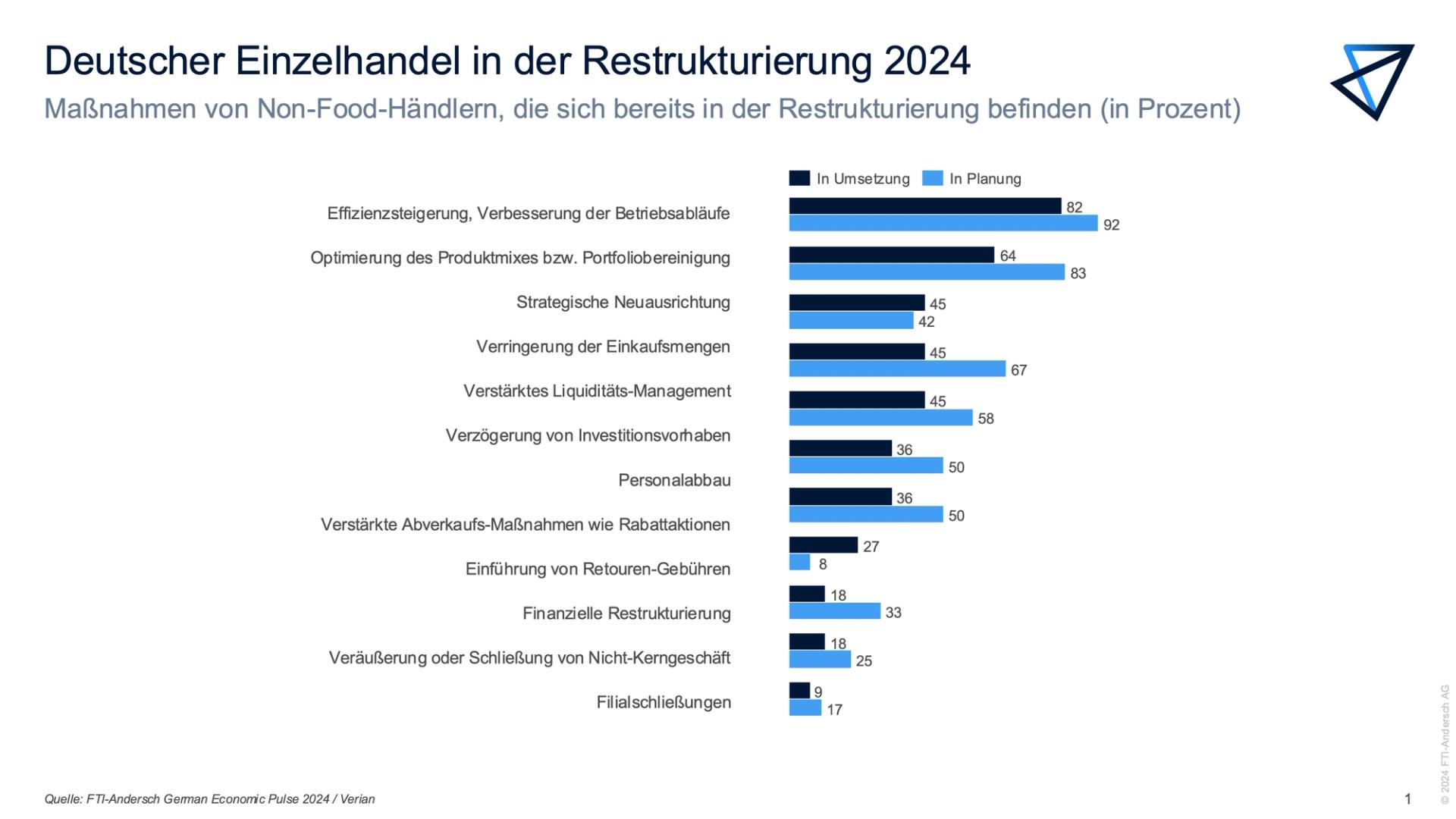

Additional measures retailers undergoing restructuring plan to address include portfolio streamlining (92%), enhanced liquidity management (67%), and postponing investments (58%). Other actions include reducing order volumes (42%) and boosting sales efforts (50%). While only 9% of respondents are currently working on store closures, 17% plan to address this in future measures. Additionally, 83% of companies with restructuring plans are considering a strategic realignment, and 64% of those already in restructuring are actively working on it.

"Stabilization and consistent realignment must occur simultaneously. Otherwise, companies lose too much time, which they no longer have," says Dorothée Fritsch. "Companies must now fundamentally determine what a stable new setup looks like. This involves not only portfolio streamlining but also thoroughly questioning strategies, structures, and processes for their value contribution. Special attention should also be given to portfolios and channels."

Immediate Action Required, but no Rash Decisions

Encouragingly, one in five (20%) retailers is already considering acquiring struggling competitors or suppliers. Additionally, 68% are working to expand their customer and partner base beyond existing markets, and 48% are intensively screening their suppliers due to current market conditions. However, only one in ten respondents is examining the financial health of their landlords.

"It will soon become clear who is well-prepared for this storm. These retailers have already focused on successful and innovative sales formats, a targeted product range, strong integration of physical stores and profitable digital channels, the right locations, and a positive customer experience," says Dorothée Fritsch.

Fritsch adds: "Other success factors we observe in the market include developing new delivery models in collaboration with key suppliers and negotiating partially flexible rental cost models with landlords. As in any crisis, there will be winners here, though significantly fewer than losers. Now is the time to keep a cool head, develop a plan, carefully distinguish between short- and long-term measures, and finally embark on the transformation that has been neglected in too many cases over recent years."

About the Verian Study:

The market research company Verian (formerly Kantar Public) conducted a study titled 'German Economic Pulse 2024' on behalf of the consulting firm FTI-Andersch. This study involved telephone interviews with 200 companies in Germany from the automotive, machinery and plant engineering, consumer goods, and retail sectors, focusing on current topics such as economic outlook, restructuring, insolvencies, refinancing, and other structural challenges.

The surveyed companies each have a minimum annual revenue of €50 million, with approximately a quarter generating more than €500 million per year.

About FTI-Andersch:

FTI-Andersch is a management consultancy that supports its clients in the development and implementation of sustainable future/performance and restructuring concepts. FTI-Andersch actively supports companies that have to deal with strategic, operational or financial challenges and transformation processes – or want to align their business model, organization and processes for the future at an early stage.

Clients include medium-sized companies and large corporations. FTI-Andersch is part of the FTI Consulting Group (NYSE: FCN), which has more than 8,000 employees worldwide.

FTI-Andersch AG

Taunusanlage 9-10

60329 Frankfurt am Main

Germany

For press inquiries, please contact:

T: +49 69 27229950

Your Contacts

Dorothée Fritsch

Dorothée FritschHead of Business Development & Strategy